Zoe Palmer

@zoe.scoretrack

CESGA candidate

“Pass CESGA gave me a cleaner way to review CESGA. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Pass CESGA provides exam-style practice questions, flashcards, mind maps, study guides, and focused review tools for ESG, sustainable finance, climate risk, governance, and responsible-investment certification, including CESGA, ACE, CCI, CIEI, CGIEP.

Practice

Question-bank drills

Review

FSRS recall scheduling

Clarity

Weak-spot analytics

Explore the certifications covered by Pass CESGA and move directly into the module that matches your exam path.

CESGA Exam

AICPA & CIMA ESG Certificate

Certificate in Climate and Investing (CCI)

CFA Institute Certificate in ESG Investing

Corporate Governance Institute ESG Professional Certificate

GARP Sustainability and Climate Risk (SCR) Certificate

GRI Professional Certification

IASE Certified ESG Practitioner (CESGP)

IASE International Sustainable Finance (ISF) Certification

International Sustainability Standards Board (ISSB) Certification

LSEG Academy Sustainable Finance Professional

SASB Fundamentals of Sustainability Accounting (FSA) Credential

UNPRI Academy Responsible Investment Certification

The platform is built to feel less like a noisy marketplace of study tools and more like one disciplined preparation desk.

Practice with questions modeled after real certification exams.

Our FSRS algorithm schedules reviews so you retain more, faster.

Simulate real exam conditions with timed practice sessions.

Detailed dashboards showing accuracy trends and topic mastery.

Recharts-powered visualizations of your performance over time.

If you genuinely need more time, we support your preparation with continued access options.

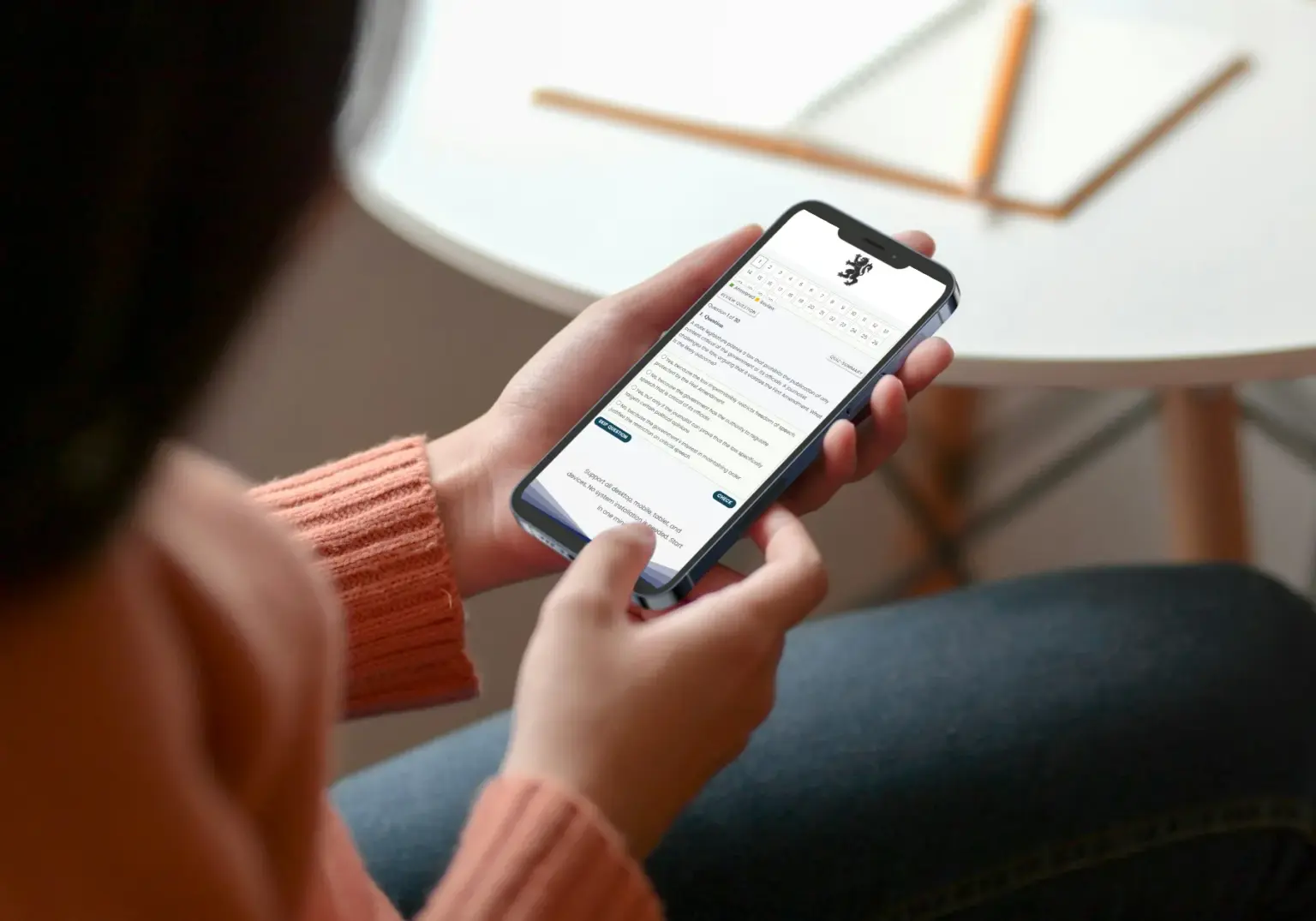

Practice on your phone during commutes, review flashcards on your tablet, or run full mock sessions on desktop. The experience is designed for candidates balancing work, family, training, and a real exam deadline.

Full access includes the question bank, timed mocks, spaced repetition, analytics, flashcards, mind maps, and companion revision assets for the certifications you choose on Pass CESGA.

A wider cross-section of candidate feedback so the site feels like a serious preparation platform, not a thin landing page.

Zoe Palmer

@zoe.scoretrack

CESGA candidate

“Pass CESGA gave me a cleaner way to review CESGA. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Daniel Hayes

@daniel.revisionrun

ACE candidate

“Pass CESGA gave me a cleaner way to review ACE. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Harper Blake

@harper.revision

CCI candidate

“Pass CESGA gave me a cleaner way to review CCI. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Mason Reed

@mason.mockdays

CIEI candidate

“Pass CESGA gave me a cleaner way to review CIEI. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Olivia Hart

@olivia.studygrid

CGIEP candidate

“Pass CESGA gave me a cleaner way to review CGIEP. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Noah Bennett

@noah.reviewstack

SCR candidate

“Pass CESGA gave me a cleaner way to review SCR. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Chloe Mercer

@chloe.passplan

GP candidate

“Pass CESGA gave me a cleaner way to review GP. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Julian Park

@julian.preprhythm

CESGP candidate

“Pass CESGA gave me a cleaner way to review CESGP. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Sofia Lane

@sofia.tracknotes

ISF candidate

“Pass CESGA gave me a cleaner way to review ISF. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Ethan Cole

@ethan.studyblocks

ISSB candidate

“Pass CESGA gave me a cleaner way to review ISSB. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Amelia Frost

@amelia.retakeplan

LASFP candidate

“Pass CESGA gave me a cleaner way to review LASFP. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Lucas Grant

@lucas.morningprep

FSA candidate

“Pass CESGA gave me a cleaner way to review FSA. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Nora Ellis

@nora.reviewlog

UARI candidate

“Pass CESGA gave me a cleaner way to review UARI. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Caleb Morgan

@caleb.mockflow

CESGA candidate

“Pass CESGA gave me a cleaner way to review CESGA. The practice questions and explanations made it much easier to see what needed another pass before exam day.”

Lily Dawson

@lily.examdesk

ACE candidate

“Pass CESGA gave me a cleaner way to review ACE. The practice questions and explanations made it much easier to see what needed another pass before exam day.”